HRA is the amount paid by the employer to employees towards the payment for accommodations every year. It is a part of salary and a way to get the income tax benefit under section 10(13A).

In this article, we are going to explain everything about HRA exemption, how to claim HRA, TDS provisions on rent, what is rental agreement.

How to claim HRA?

To avail the HRA exemption, few conditions are needed to be fulfilled by the employer:

- The employee should live physically in the rented property. In case of making payment of rent to the parents, your parents should mention the rental income in their ITR.

- Employee has to submit its rent receipts or rent agreement with the contents as mentioned below to the employer.

- Quoting the PAN number of the landlord is mandatory if your rental expense is more than Rs. 1 lakh in a year. In case, the landlord doesn’t have a PAN number; he has to submit a declaration in Form -60.

- Make sure to make rent payments through banking channels as it helps to establish valid proof of making rent payments.

- The employer would calculate HRA exemption based on your salary, and it shall be reflected in Form – 16 on timely submission on rent receipts or rent agreement.

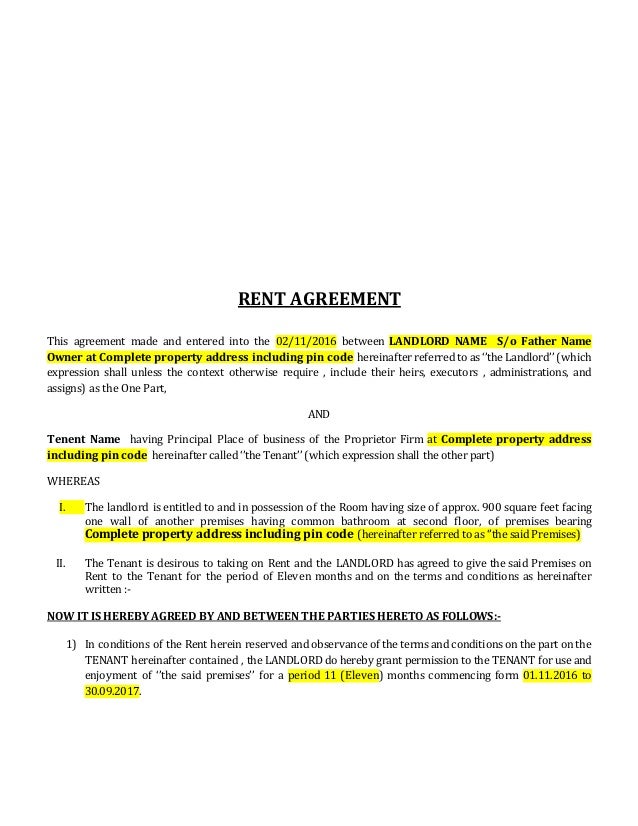

Rental agreement:

Based on various tribunal case laws decided in April 2017, it is said that to claim the HRA exemption, the employer must have to rent agreement and rent receipts. Although the rent agreement is not mandatory to submit to claim HRA exemption, the reason behind this is; it serves the genuine evidence (rent agreement) to claim HRA.

Rent agreement is a legal written document between the tenant and the landlord of the property. This document binds both the parties to fulfill their obligations and also provides safeguards the interest of both the parties.

Notary: In India, if your rental agreement is printed on the stamp paper, then it is not mandatory to notarize a rental agreement. However, it must be signed by both parties and two witnesses

Stamp Paper: The Indian Law mandates some payments to be made to Central to State government on specified kinds of payments. Buying and selling real estate is one of the specified transactions on which “Stamp Duty” is paid to the government for the rental agreements. The price of stamp duty (Rs. 20, 50, or 100) varies from state to state as per the Indian Stamp Act. Nowadays, E-Stamping is the easiest way for the payment of stamp duty to the government.

Revenue Stamp: If you are making payment of rent in cash more than Rs. 5,000 then, you need to affix revenue stamp on rent receipts. However, it is not required in case of online or cheque payment.

Contents of the rental agreement:

The rent agreement specifies the terms and conditions based on which property is let out to the tenant. Most rent agreements are signed for the standard period of 11 months.

- Personal details of both parties (Name, Address and Spouse Name)

- Description of the property (address, type, and size)

- Monthly rent

- Due date of payment of rent (penal charges in case of delay)

- Security deposit by the tenant

- Use of property (Residential or commercial)

- Duration of the tenancy

- Party responsible for damages like ceilings, rooftop

- Renewal and notice period

- Agreement terminated conditions

- Signature and Date

These are the things generally contained in a rent agreement. However, both parties are free to add more clauses like other facilities parking, electricity expenses, and society’s membership, etc. to brief the agreement on their mutual understandings.

Here is a sample of Rent agreement for your reference. There is no specific format for the rent agreement. You can prepare the rent agreement online with the help of some legal advisory like legaldesk.com, edrafter.in, notarykar.com, etc.

TDS provisions on rent of property:

All individuals and HUF paying monthly rent in excess of Rs. 50,000 is liable to deduct TDS under section 194B. The rate of TDS shall be Rs. 5%.

- In case you forgot to deduct TDS, interest shall be levied @1% per month and

- Non-deduction of TDS attracts the interest and penalty in the following manner:

- In case of TDS deducted but not deposited, interest shall be levied @ 1.5% per month

- The penalty shall be Rs. 200 per day until the delay continues.