The newest twenty eight% financial code

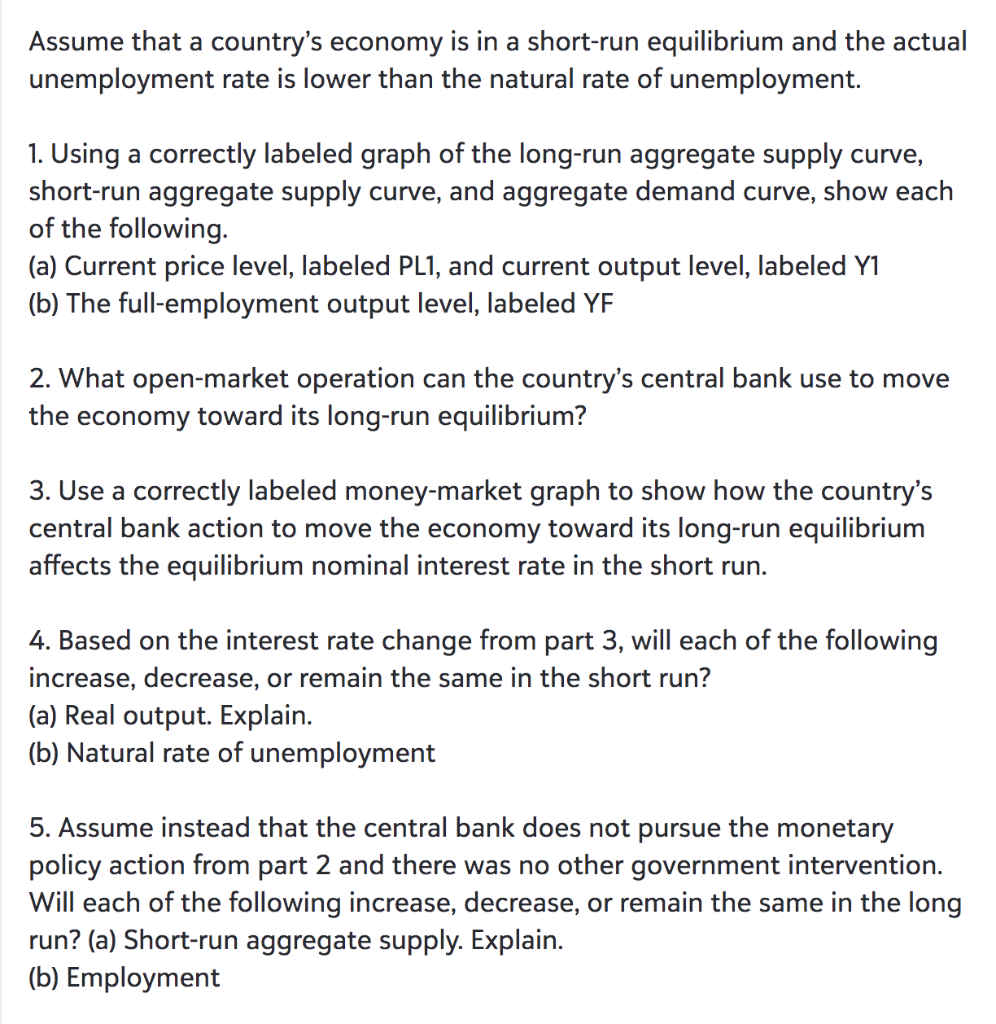

The recommended figure that all lenders and you will assets gurus wanna bandy on the was twenty-eight% away from pre-tax earnings. Which means no more than 28% of your own gross monthly money should go to your month-to-month financial cost.

- Example according to monthly earnings: In case your pre-income tax monthly money was $9,000, you should not shell out over $dos,520 towards your financial every month. You will find you to definitely count by the multiplying the monthly pre-taxation earnings ($nine,000) from the 28% (0.28).

- Analogy predicated on financial dimensions: If you would like borrow $500,000 to own a simple 29-season mortgage that have a good 5.89% interest rate, you’d need secure at the least $10, per month – otherwise a $127, salary – to pay for new $dos,972 monthly repayment.

Home loan worry threshold

- Analogy centered on month-to-month income: Should your https://paydayloanalabama.com/blountsville/ monthly pre-tax income try $nine,000, you need the month-to-month money to keep below $2,700.

- Example predicated on financial size: Regarding same fundamental $500,000 mortgage, you’d need earn at the least $nine, month-to-month – or a beneficial $118, income.

Since the an initial homebuyer, you may have a lot to consider and you will high on the new checklist are going to be what size financial you could rationally pay, not how much cash you might borrow, because they’re both various other.

Debt-to-earnings proportion

A mortgage-to-money proportion tend to clearly indicate exactly how much you need to dedicate to the home loan while keeping a boundary against unforeseen situations. Just like the a primary house visitors, a different sort of signal you to definitely loan providers will on directly will be your debt-to-earnings (DTI) ratio.

DTI form the total amount of loans might hold whenever you are taking aside home financing against your earnings. Income include normal money off financial investments, employment, overtime functions, incentives and you may returns of shares. Loans could feature from handmade cards and personal funds so you can tax expenses and purchase now, shell out later finance.

To track down the DTI, split your debt by your revenues. For example, state we need to borrow $800,000 to find property. You will also have good $twenty-five,000 car loan and $20,000 during the credit debt. Your own full debt would-be $845,000. Should your revenues was $150,000, your debt-to-money ratio is actually $845,000 ? $150,000. That’s 5.63% otherwise 5.63 DTI.

All the way down DTIs are more effective, and better ratios makes protecting the borrowed funds you will need more challenging. But not, just like the you don’t really want to use over your are able to afford, which is perhaps not bad. You can reduce your DTI because of the rescuing a top put or paying off most other costs, particularly handmade cards.

What is actually good obligations-to-income ratio having home financing?

- A beneficial DTI out-of 3 otherwise less than is excellent

- An effective DTI away from four to six excellent not high

- A DTI over seven could be experienced risky.

Australian loan providers features tightened the financing criteria once the pandemic and you may features clamped off particularly difficult on higher DTI rates. The major Five banks are common somewhere within eight and 8 – according to variety of financing plus the number you desire so you can borrow.

Yet not, lenders including usually look at your individual circumstances. So, DTI advice aren’t fundamentally place in stone. Lenders may recommend the job on the borrowing divisions for remark or provide you with more flexibility – like, when you have an effective guarantor.

Your budget

One of the recommended an easy way to figure out what portion of your revenue you would certainly be safe planning to your home loan is with a straightforward funds. That it begins with factoring on your own month-to-month expenses and you will any money you to definitely continuously is inspired by your account.

People, especially those rather than pupils and with a combined financial, is put more than 29% of its wages to their mortgage and still alive easily versus actually upcoming near to home loan be concerned. Of a lot residents need to pay off the financial as fast as possible. Thus, they’re delighted paying up to help you fifty% of their money to their financial, no less than for most age.

Making a spending plan usually still give you a better sign of what you are able rationally pay for. If you find yourself leasing, that will give you some idea of the place you will most likely become once your financial begins.

What’s normal to own a mortgage in australia?

Assets rates across the country has actually grown of the a massive 23.6% given that , position the common holder-occupier possessions within $593,000 from inside the . Up until very has just, historically lowest pricing possess kept financial worry from increasing. not, there were a dozen interest rate nature hikes since that time. Very, the impression out of mortgage payments to the home spending plans was in limelight once more.

Slightly alarmingly, a recent statement discovered more than 1.43 million mortgage owners (twenty eight.7%) happen to be sense mortgage worry otherwise prone to financial be concerned.

A great deal more distressing try research out of ANZ CoreLogic throughout the Casing Value, hence discovered that mortgagees, typically, wanted to save money than just forty% of its income so you’re able to solution its mortgage loans. That is means over the twenty eight% home loan rule and you may stress tolerance.

Ideas on how to decrease your home loan repayments

Consider, a mortgage can work on for up to 30 years, as well as your money is extremely planning change-over that time because of a variety of issues. Thank goodness, you could require some strategies to lower the home loan repayments when you look at the a crisis.

- Get hold of your bank immediately. First, you should get hold of your financial and communicate with them. While you are unsure what you should state, you can buy a brokerage to speak with them on your part. The bank need to have a range of choices for your, with regards to the dimensions and you may period of your home loan. They likewise have difficulty principles that’ll help you to get straight back on the foot. Just be careful you to definitely even though some of your lender’s possibilities normally enable you to get off a primary pickle, they may ask you for alot more finally.

- Refinance the loan. Depending on how enough time you have had your own mortgage, you have some security about property. That allows one refinance your loan to possess greatest words and you may standards probably.

When you are a recent resident incapable of pay their month-to-month financing, you are sense mortgage fret. Capture any kind of actions available for you to lessen your own month-to-month repayments whenever you can.